A Payday For Payloads: The Transactional Landscape Of ADCs

By Trent Gordon, M.S., Mavra Nasir, Ph.D., and Peter Bak, Ph.D., Back Bay Life Science Advisors

With 12 FDA-approved antibody-drug conjugates (ADCs), three of which have already reached blockbuster status, the future of targeted cytotoxic therapy is upon us. Since the first ADC approval of Mylotarg (gemtuzumab ozogamicin) in 2000, there have been numerous advances in the discovery, development, and manufacturing of ADC technology, allowing for the development of increasingly potent ADCs with a reduced toxicity profile.1 Given the keen interest in the field and high-profile M&A discussions, we assessed the evolution of the ADC transaction and financing landscape. In the last five years, ADCs have commanded the highest deal value relative to any other technology in oncology, with the average overall deal value for ADCs exceeding $2 billion. The majority of ADC transactions were for discovery and preclinical stage assets that were able to demonstrate robust anti-tumor efficacy in xenograft models across tumor types.

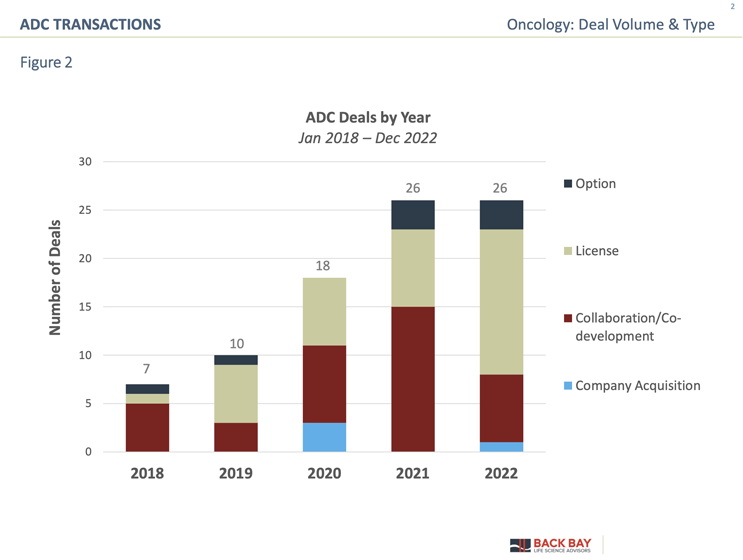

The volume of ADC transactions has increased over threefold since 2018, and 2022 closed out with three ADC transactions in the last two weeks of the year. Given the notable efficacy, commercial success, and potential for a longer exclusivity runway, it is no surprise ADCs have been the darling of the oncology space.

Early-stage ADC Deals Signal Industry Confidence

The transaction landscape in oncology has been dominated by small molecule therapeutics, which have been the mainstay of cancer treatment since the first documented use of chemotherapy in 1946 2 (Figure 1). With the advent of monoclonal antibodies (mAbs), immune-targeted treatments (e.g., checkpoint inhibitors, adoptive cell therapy, CAR-T), and cellular therapies, there has been substantial deal flow for novel modalities. While fewer in frequency relative to other novel modalities, there has been an acceleration in ADC transactions, typically focusing on assets/companies in early stages of development.

Since 2018, there has been over a threefold increase in deal volume for ADC-related assets (Figure 2), and partner interest may have been driven by the approval of eight different ADCs during that timeframe (excluding Blenrep due to its withdrawal from the market in 2022):

- Lumoxiti, 2018

- Polivy, 2019

- Padcev, 2019

- Enhertu, 2019

- Trodelvy, 2020

- Zynlonta, 2021

- Tivdak, 2021

- Elahere, 2022

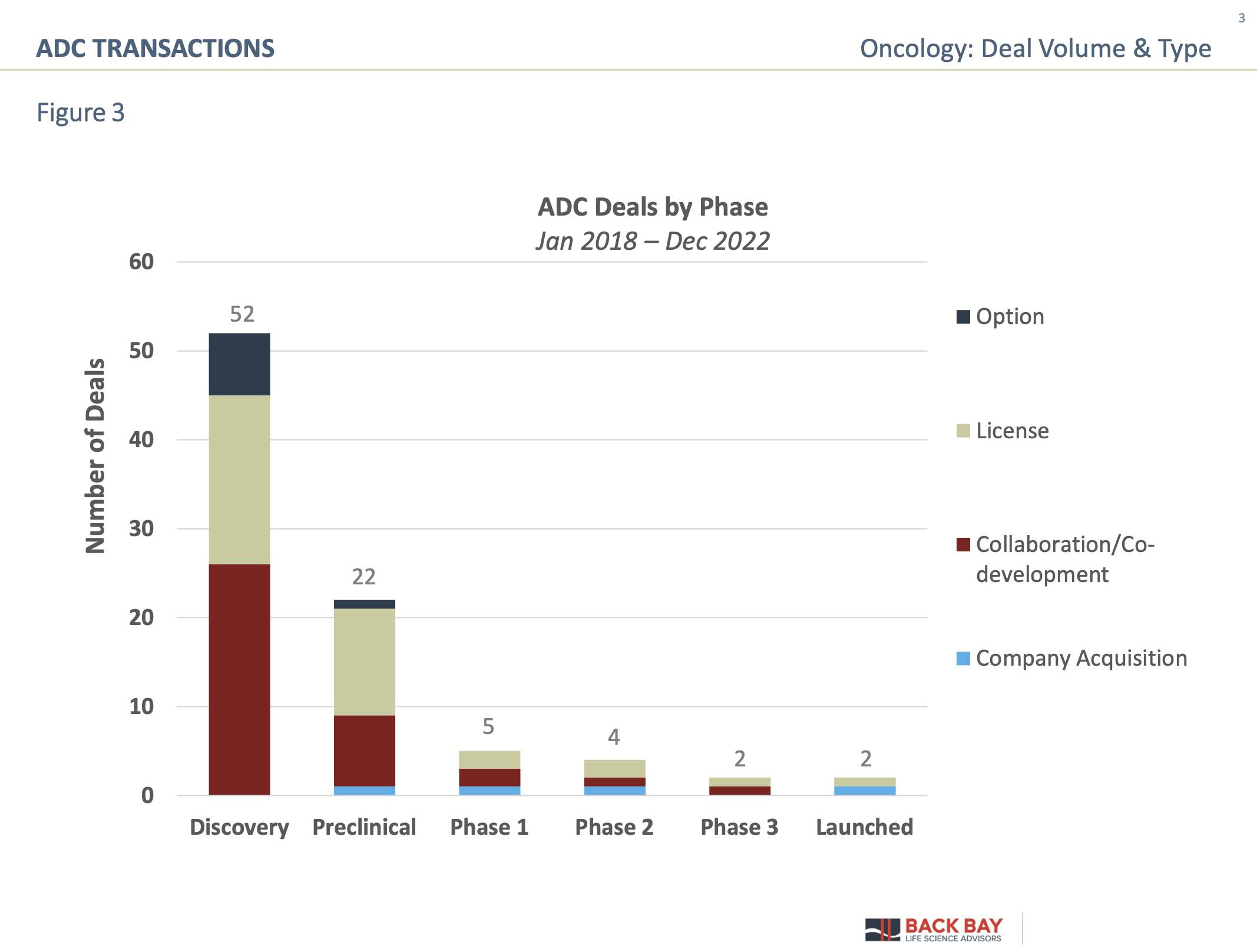

Currently, there are more than 500 industry-sponsored active clinical trials involving more than 140 unique ADCs, which is expected to result in continued interest and subsequent transactions in the space. To close off 2022, there was particular interest in ADCs from large pharma, with Merck executing two deals and Amgen initiating an ADC transaction during the second to last week of the calendar year. Notably, ADC deals are frequently struck early in the product development life cycle. When analyzing ADC transactions based on the phase of development (Figure 3), there is a clear appetite for early-stage technologies/assets, particularly at the discovery phase. Early-stage discovery transactions have predominantly focused on developing the mAb portion of the ADC to allow for improved targeting and optimization with linker chemistry to enhance ease of manufacturing.

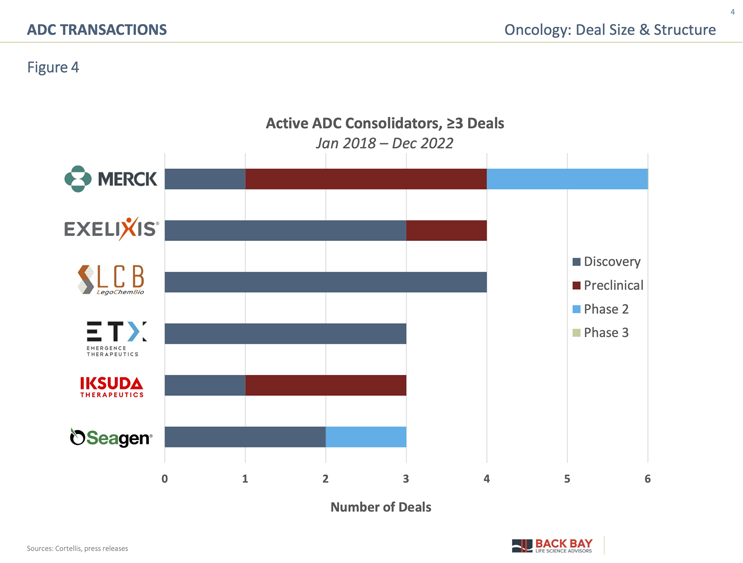

Active consolidators in the space span global biopharma with a diverse oncology portfolio to those with a dedicated ADC focus (Figure 4). While Merck is known in oncology for its market-leading immune-oncology product, Keytruda, it has broadened its oncology portfolio with a focus on ADC business development. Merck’s ADC transactions include its $2.8 billion acquisition of VelosBio in 2020 and a $9.5 billion preclinical multi-asset acquisition deal in 2022 with Sichuan Kelun (Appendix Figure 1), as well as the rumored $40 billion failed acquisition of Seagen. Seagen is broadly regarded as the industry leader in ADCs, with three commercial ADCs (Adcetris, Padcev, and Tivdak) and more than 10 ADCs in its clinical development pipeline. Seagen’s in-licensing actives have focused on acquiring early-stage ADCs and subsequent antibodies, while its Phase 2 license involved a novel HER2-targeted ADC, disitamab vedotin, potentially indicating its desire to enter the blockbuster HER2 targeted space currently occupied by Kadcyla and Enhertu.

Exelixis, a commercial-stage oncology company, has recently added two ADCs to its pipeline and after $82.5 million in option and licensing fees to Iconic Therapeutics has successfully taken its ADC into Phase 1 development (Appendix Figure 2). The remainder of active consolidators have focused on bolstering their ADC development capabilities with early-stage transactions. While not typical consolidators, Iksuda (Series A, 2021, $47 million) and Emergence Therapeutics (Series A, 2021, $98 million) are both pure-play ADC companies, with cash in hand and looking to build out a differentiated ADC pipeline. LegoChem is both an active out-licenser of ADCs assets and a collaborator/in-licensor of ADC assembly technology from companies such as Mediterranea Theranostic Srl, NextCure, and Glycotope to expand its own development capabilities.

Potential Means Big Payouts In ADC Acquisition Landscape

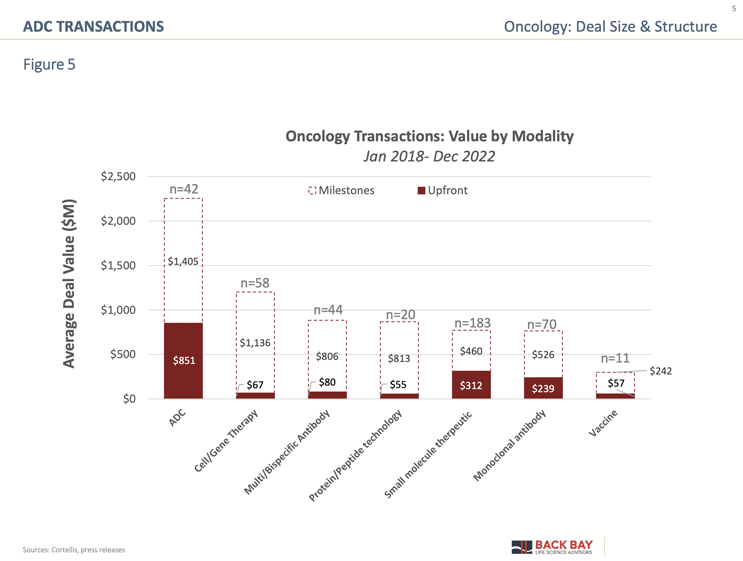

While less frequent than other modalities, ADCs have commanded the highest deal value relative to any other modality (Figure 5). On average, the up-front deal value was $851 million across all stages (based on 42 disclosed deals) and, of those, five deals offered >$1 billion up front. When evaluating median value, the overall value for ADCs is $848 million, which is >$300 million more than the $512 million median for multi/bispecific antibodies. What is particularly striking about the transaction landscape for ADCs is the large overall deal value across stages of development (Figure 6). While there is a consistent increase in overall deal value from preclinical through Phase 3 (~$2 billion in preclinical to ~$4 billion for Phase 3), there is a significant increase in up-front value (tenfold increase from $52 million in preclinical to $520 million in Phase 1), demonstrating the value of de-risking the asset with safety and clinical data.

The multibillion-dollar milestone payments offered for preclinical and clinical-stage assets are relatively unique to the ADC landscape. These large milestone payouts are likely due to the extended blockbuster potential of ADCs, which, because of challenges with biosimilar manufacturing, can continue beyond the drug’s patent life. There is a significant jump in up-front value for launched assets, which is driven by Gilead’s $21 billion acquisition of Immunomedics. The acquisition was centered around the ADC Trodelvy, which analysts projected would reach $4 billion in peak sales solely in triple-negative breast cancer (TNBC). Trodelvy was approved in TNBC five months prior to the acquisition in September 2020 and generated $20.1 million in revenue during its first two months on the market. The other disclosed commercial-stage deal involved a licensing agreement for Sobi to develop and commercialize ADC Therapeutics’ Zynlonta in Europe and select international territories for $55 million up front with the potential to receive up to $435 million in milestones. Despite the seemingly large value for commercial-stage deals, the total value could have been further increased had the rumored $40 billion merger between Merck and Seagen not fallen through because of pricing negotiations.

To cap off the excitement around ADCs in the past five years, 2022 ended the year with a very large ADC biobucks-centered deal between Merck and Kelun-Biotech for seven preclinical ADC candidates, valued at $175 million up front and up to $9.3 billion in milestone payments.

Unique Market Profile Makes ADCs An Attractive Investment

Looking forward, as the clinical pipeline matures, the next wave of innovative biotech companies within the ADC space has raised venture capital (VC) funds and is looking to enhance the therapeutic window of ADCs without compromising safety or stability.

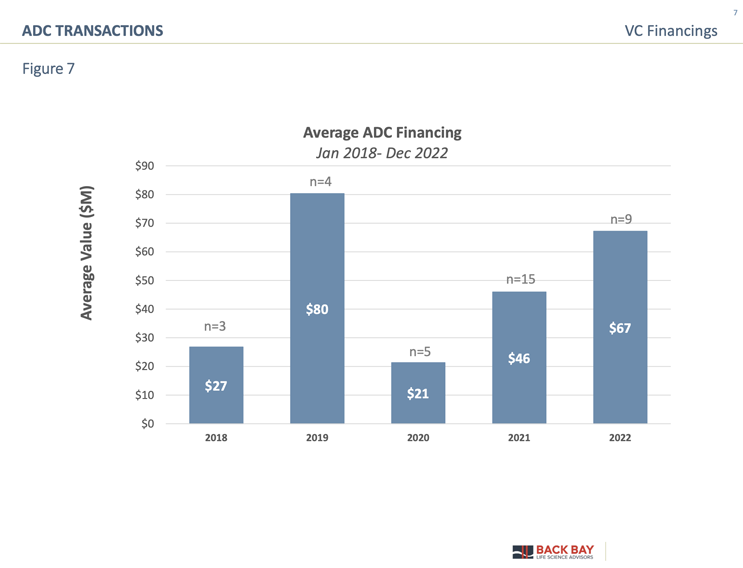

VC funding for ADC technologies has steadily increased since 2018, with an aggregate of about $1.8 billion invested by the end of 2022 (Figure 7). A significant inflection in average deal value ($80 million, n = 4) occurred in 2019 following the approval of three ADCs in that year (Polivy/Roche, Padcev/Seagen, and Enhertu/Daiichi Sankyo, AstraZeneca).

Another milestone was achieved in 2021, with a record number of financings (3.5-fold increase compared to 2019) following four additional approvals in 2020-21 (Trodelvy/Immunomedics, Blenrep/GSK, Zynlonta/ADC Therapeutics, Tivdak/Seagen) and the unfolding commercial success of already approved ADCs (Figure 7). The healthy landscape of early-stage biotech companies as well as heightened interest from pharma holds great promise for actualizing the true potential of this magic bullet modality as a targeted therapy.

When considering why ADCs have had such success in the transactional space, we hypothesize there are three major drivers to deal value:

Efficacy

ADCs have demonstrated improved targeting of cytotoxic agents through increased tumor specificity and selectivity, which limits systemic exposure and increases cytotoxic potency. Due to ADCs’ targeted nature, their durability is increased relative to traditional chemotherapy, as they can deliver increased doses of cytotoxic agents directly to the tumor site.

ADC assets that successfully underwent preclinical transactions often demonstrated an ability to reduce tumor volume in multiple xenograft models and were differentiated in their target. For example, GSK’s option agreement with Mersana Therapeutics for $100 million up front and $1.36 billion in milestone payments was driven by XMT-2056’s efficacy in reducing tumor volume in both HER2-high- and HER2-low-expressing models and its novel STING targeting pathway (Appendix Figure 3). As successful ADCs progressed through the clinical stage, the excitement around their efficacy increased and may be best exemplified by the standing ovation that Enhertu received at ASCO 2022 for its Phase 3 DESTINY-Breast04 trial, where it showed a 4.8-month improvement in progression-free survival and a 6.6-month improvement in overall survival.

Commercial Success

Launched ADCs have seen significant returns for sponsors as three out of the 12 approved ADCs, Kadcyla (Roche), Adcetris (Seagen), and Enhertu (Daiichi Sankyo), have reached blockbuster status with 2022 sales of $2.2 billion, $1.4 billion, and $1.2 billion, contributing to 5%, 49%, and 15% of total company sales, respectively. 4

Exclusivity

ADCs are unique among biologics with respect to the market exclusivity they might command. One of the primary challenges that ADC developers undergo is the difficulty in manufacturing, particularly the conjugation of the antibody to the highly active cytotoxic component. The conjugation chemistry introduces further heterogeneity across ADCs and must be addressed with additional assays to assess the drug-to-antibody ratio and amount of free/bound cytotoxic drug. In order to develop biosimilars of an already complicated process, manufacturers must invest large amounts of capital to purchase specialized containment equipment, introduce advanced assay systems, and learn to apply advanced conjugation techniques to differentiated biological material, all while ensuring strict homogeneity across batches.

The manufacturing barriers make it challenging for biosimilar development, although not impossible, given that Zydus Cadila was able to produce the first biosimilar ADC of Kadcyla. However, given these significant manufacturing hurdles, we expect ADC biosimilar development to remain an anomaly rather than the industry norm.

References:

- Drago, J. Z., Modi, S. & Chandarlapaty, S. Unlocking the potential of antibody–drug conjugates for cancer therapy. Nature Reviews Clinical Oncology vol. 18 327–344 Preprint at https://doi.org/10.1038/s41571-021-00470-8 (2021).

- Falzone, L., Salomone, S. & Libra, M. Evolution of cancer pharmacological treatments at the turn of the third millennium. Frontiers in Pharmacology vol. 9 Preprint at https://doi.org/10.3389/fphar.2018.01300 (2018).

- Rome, B. N., Lee, C. C. & Kesselheim, A. S. Market Exclusivity Length for Drugs with New Generic or Biosimilar Competition, 2012–2018. Clin Pharmacol Ther 109, 367–371 (2021).

- Evaluate Pharma

- Databases: Cortellis, Pitchbook, TrialTrove, PharmaProjects

About The Authors:

Trent Gordon is senior analyst at Back Bay Life Science Advisors, providing strategic and investment banking guidance to life sciences companies. He worked as a product engineer with Abbott Laboratories where he developed point-of-care blood testing assays. During his time at Back Bay, Gordon has worked on consulting and transaction-related engagements across therapeutic areas including oncology, autoimmune, and rare disease. His engagements have ranged from go-to-market strategy, early pipeline prioritization, and financing and transactional support. He holds a B.Eng. in biochemical engineering and an M.S. in biomedical engineering from Western University. Connect with the author at www.bblsa.com.

Trent Gordon is senior analyst at Back Bay Life Science Advisors, providing strategic and investment banking guidance to life sciences companies. He worked as a product engineer with Abbott Laboratories where he developed point-of-care blood testing assays. During his time at Back Bay, Gordon has worked on consulting and transaction-related engagements across therapeutic areas including oncology, autoimmune, and rare disease. His engagements have ranged from go-to-market strategy, early pipeline prioritization, and financing and transactional support. He holds a B.Eng. in biochemical engineering and an M.S. in biomedical engineering from Western University. Connect with the author at www.bblsa.com.

Peter Bak, Ph.D., is a managing director at Back Bay Life Science Advisors where he focuses on liquidity planning and positioning, strategic franchise building, mergers and acquisitions, and licensing strategy. He earned his Ph.D. in microbiology and immunology at Dartmouth Medical School where his research uncovered novel pathways of immunosuppression in ovarian cancer. He later studied as an American Cancer Society post-doctoral fellow at MIT's Koch Institute of Integrative Cancer Research. At MIT, Bak focused on the development of immunotherapies for prostate cancer and led projects with researchers from the departments of biological and chemical engineering.

Peter Bak, Ph.D., is a managing director at Back Bay Life Science Advisors where he focuses on liquidity planning and positioning, strategic franchise building, mergers and acquisitions, and licensing strategy. He earned his Ph.D. in microbiology and immunology at Dartmouth Medical School where his research uncovered novel pathways of immunosuppression in ovarian cancer. He later studied as an American Cancer Society post-doctoral fellow at MIT's Koch Institute of Integrative Cancer Research. At MIT, Bak focused on the development of immunotherapies for prostate cancer and led projects with researchers from the departments of biological and chemical engineering.

Mavra Nasir, Ph.D., is a senior consultant at Back Bay Life Science Advisors where she supports strategic engagements across a range of therapeutic areas, including rare diseases, hematology and oncology, and metabolic diseases for the biopharma and medtech industries. Nasir earned her Ph.D. in quantitative biomedical sciences from Dartmouth College. She published research in non-invasive infectious disease diagnostics using advanced mass spectrometry and machine learning, which she presented at national and international conferences. She received her B.S. in biological sciences from McGill University and M.S. in bioinformatics from New York University.

Mavra Nasir, Ph.D., is a senior consultant at Back Bay Life Science Advisors where she supports strategic engagements across a range of therapeutic areas, including rare diseases, hematology and oncology, and metabolic diseases for the biopharma and medtech industries. Nasir earned her Ph.D. in quantitative biomedical sciences from Dartmouth College. She published research in non-invasive infectious disease diagnostics using advanced mass spectrometry and machine learning, which she presented at national and international conferences. She received her B.S. in biological sciences from McGill University and M.S. in bioinformatics from New York University.